Overview of Agribusiness Financing Landscape in Nigeria

Agribusiness in Nigeria, encompassing farming and related activities, plays a crucial role in the nation's economy by contributing significantly to GDP and providing substantial employment. Despite its importance, the sector faces major financing challenges. Agribusiness financing, which includes loans, credit lines, guarantees, and grants, is essential for boosting sector output and ensuring food security. However, the sector is under-financed due to perceived high risks. These risks stem from several sources: the unpredictable nature of agricultural production due to dependence on weather conditions, the volatility of commodity prices, and the vulnerability of agricultural assets to pests, diseases and natural disasters. Compared to other sectors like oil and telecommunications, agriculture receives less than 5% share of credit despite accounting for a quarter of economic output. This under-financing leaves Nigerian agribusinesses struggling to secure funds for expansion, technology investment, and daily operations. With a financing gap estimated at N76 trillion (USD 183 billion), developing robust and accessible funding systems is increasingly critical.

What are the Key Challenges Faced by Agribusinesses in Accessing Finance?

Agribusinesses face significant challenges in accessing finance due to several critical factors:

- Risk Perception: Financial institutions often view agriculture as high-risk, particularly in countries like Nigeria where agriculture is rain-dependent, lacks adequate storage, and insurance options. The seasonal revenue fluctuations and unpredictable market demand further exacerbate this risk, making lenders hesitant and leading them to demand higher debt repayment rates that many agribusinesses, especially SMEs, cannot afford.

- Operating Structures: Many agribusinesses operate like small shops with poor accounting practices and a lack of transparent financial records, making it difficult for financial institutions to assess their profitability and cash flow. This creates mistrust among potential lenders.

- Financial Literacy: Many agribusiness holders struggle with preparing business plans, conducting financial forecasting, and understanding loan terms, which not only hampers their ability to secure funding but also affects their management of any funds obtained.

- Collaterals: Many agribusinesses, particularly SMEs, lack the necessary collateral, such as formally registered land or guarantors, to secure credit from banks. Without sufficient collateral, they are unable to meet the stringent requirements set by lenders.

- Product differentiation and Pricing Strategy: The absence of clear product differentiation and a sound pricing strategy, combined with price volatility, makes it difficult for agribusinesses to present a stable financial picture to lenders, affecting perceptions of their profitability, viability, and market competitiveness.

- High-Interest Rates: High-interest rates, driven by high country risk premiums, the perceived risks of the sector, and recent increases in the monetary policy rate (MPR), reduces the capacity of agribusinesses to repay loans, creating a significant barrier to accessing finance.

Funding Sources for Agribusinesses

To improve your chances of securing funding as an agribusiness owner, it's crucial to understand the different funding sources available and their specific requirements. Each option has its own advantages and drawbacks, so grasping the complexities and prerequisites of each is essential for obtaining the capital needed for growth and sustainability.

- Bootstrap: It is a form of equity financing which involves self-financing, re-investing profits, or borrowing from family and friends. The beauty of this method lies in its simplicity — no complex applications, just a matter of trust and strong relationships. However, it is limited by the size of your personal network and savings, which may not be sufficient for scaling your business.

- Grants: Typically this is referred to as "free money" — funds that don’t need to be repaid. These can come from government programs or private organisations offering innovation grants to SMEs. But accessing these funds often involves special requirements like gender, aligning with national policies, a solid business model, and showing that your business is in good hands. Sources of these funds include the U.S. African Development Foundation (USADF), Nourishing Africa which offers up to ₦3.5m, GAIN Micro Grant for Empowerment, and AYuTe Africa Challenge. While the money is great, the application process can be tedious, with slow disbursement times and conditions attached to how you can use the funds.

- Debt: Unlike popular opinion, debt (loans) isn’t a bad thing for agribusinesses, especially if utilised properly. In fact, SMEs need debt financing to scale their businesses and improve their financial performance. Debt acts as leverage, allowing you to amplify your returns. However, it is important not to be over leveraged. A general rule of thumb is ensuring that your debt servicing to income ratio is below 25%. This means that for every hundred naira (₦100) your business earns, you should aim to spend no more than 25 naira (₦25) on paying off debt. Debt options can be concessional or market-based.

- Concessional debts include low-interest loans from government initiatives like the Commercial Agriculture Credit Scheme (CACS) and cooperative loans. Cooperative loans are relatively easy to secure as long as you’re an active member and have a good savings history with the group. They’re great if you need quick, small-scale financing, but not much is expected from this route. On the other hand, other concessional loans require a more substantial commitment — you’ll need collateral, a proven business track record, and a solid repayment plan.

- Market-based or commercial loans are excellent for funding large projects, but they come with higher interest rates and require collateral. Securing these loans requires certain key elements to demonstrate capacity, requiring expert guidance and insights.

- Early-stage equity: This funding type is ideal for early-stage innovative ventures (a scalable, high-potential business) because it doesn’t involve debt — you’re not obligated to repay the money. However, the challenge is access. It typically involves private equity and venture capitalists. Investors in equity funding seek businesses with disruptive potential, a strong management team, and a clear exit strategy. And in getting this type of funding, be prepared to give up some control over your business.

- Other equity: At the other end, Initial Public Offering (IPO) is another means of equity funding. IPO is a medium that offers large-scale funding by selling a portion of business ownership to public investors. However, it is only accessible to highly successful businesses that are ready to leap to the next level. Going public provides a substantial influx of capital for scaling and expansion, but it requires a proven track record of financial performance, strong corporate governance, and a willingness to cede significant control and transparency to shareholders.

- Non-traditional funding: Under this funding type, options like supply chain partnerships, collateralization, and crowdfunding exist. These mediums are a bit complex — some are innovative, like outgrower models or invoice trading, which can provide flexible financing tailored to specific needs. But they come with mixed expectations and are still evolving, sometimes making them a bit challenging to explore. Mostly, it requires reputation, long-term commitment and partnership management.

Each funding system has its place in the agribusiness sector. The aim is to match the right funding source to your specific needs and circumstances. By doing so, agribusiness owners can strategically close the financing gap and unlock the growth potential of their ventures.

Choosing the Right Sources of Financing for your Agribusiness

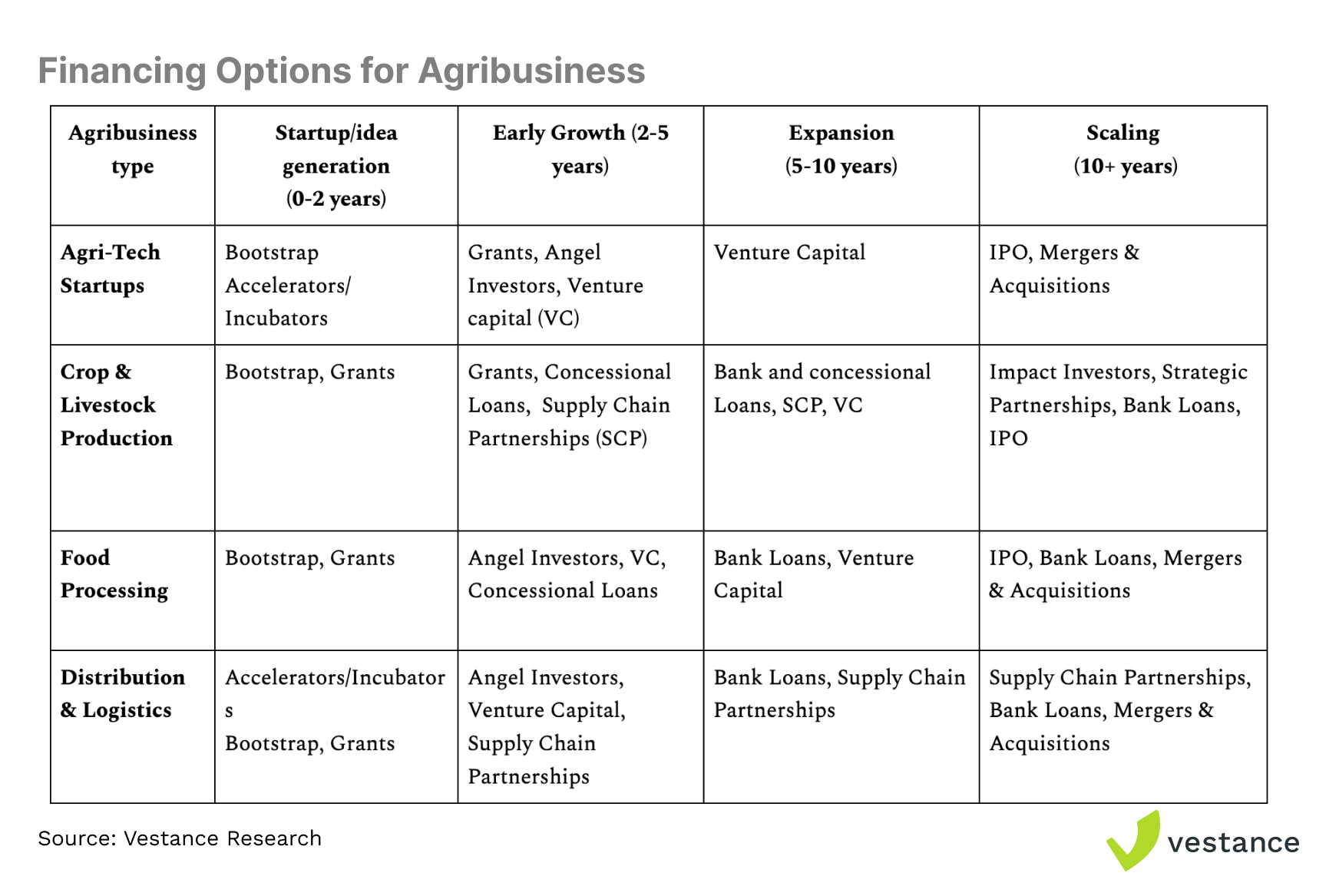

When selecting the right financing source(s) for your agribusiness, it’s essential to align your funding strategy with your business’s growth phase and specific needs. This stage-based approach ensures that the capital you raise is appropriate for where your business currently stands and where it’s headed. Stage-Based Financing involves matching your funds to your business’s growth phases — whether you’re in the startup stage, early growth, expansion, or scaling. Each phase has its own capital requirements, and the financing sources you choose should reflect this.

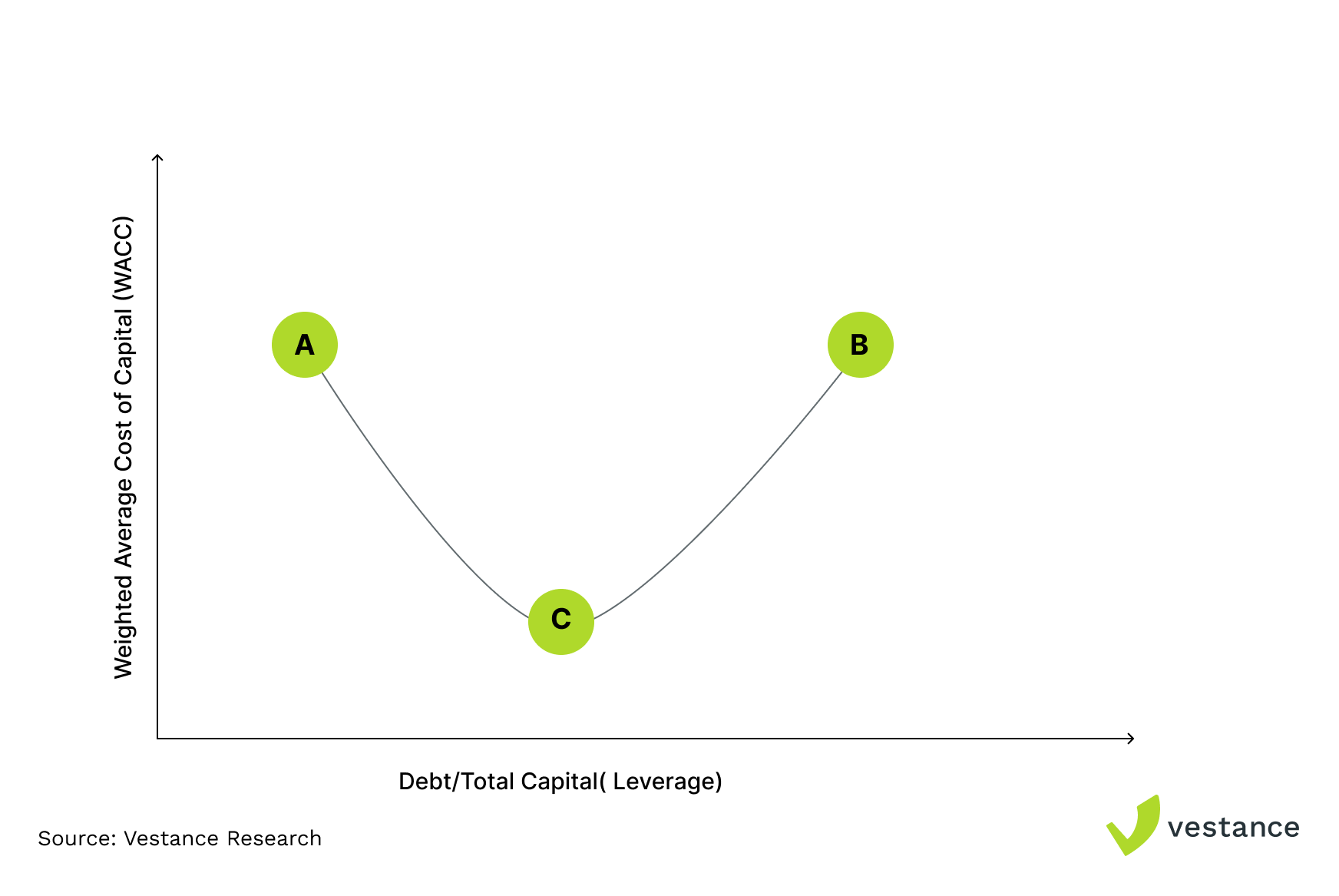

The concept of Optimal Capital Theory comes into play here, where the goal is to minimise the overall cost of capital (WACC) while maximising returns. This involves striking a balance between debt and equity financing to optimise your capital — ensuring you have enough resources to meet both long-term investment and short-term obligations without overburdening your business with excessive costs.

Before choosing a financing source, several key questions must be answered:

- Cost of Capital: What is the interest rate or required rate of return? This directly impacts your profitability and should be carefully evaluated.

- Repayment Terms: Are they favourable or restrictive? Consider whether the terms are short-term or long-term, and if there’s a moratorium period that gives you breathing room before repayment begins.

- Stage of Your Business: Are you a startup, or are you in an expansion phase? The stage dictates whether you should pursue, for example, venture capital (ideal for startups) or a commercial loan (better suited for established businesses).

- Fund Utilisation: Are you funding capital projects or working capital? Short-term loans should generally not be used for long-term projects — match the loan duration to the project’s lifespan.

- Conditionalities: Are you comfortable with the lender’s conditions, such as restrictive covenants or performance targets? These can limit your business flexibility.

- Control: How much control are you willing to give up? Equity financing might require you to cede some control to investors, whereas debt financing typically leaves you in control, though with repayment obligations.

- Application Process: Is the process cumbersome, and do you need the funds urgently? Some financing options have long approval times that may not align with your needs.

- Exit Strategy: How will you exit the financing arrangement? Whether it’s paying off a loan or eventually buying back equity, having a clear plan is imperative.

So what are your options?

Case Studies: Success Story in Agribusiness Financing

- Psaltry International – Concessional Financing (Early growth phase)

Psaltry International Limited is a successful Nigerian company specialising in the production of food-grade starch, high-quality cassava flour, and cassava-based sorbitol. The company sources cassava both from its own farms and from over 5,000 local smallholder farmers within its location, emphasising the importance of proximity to raw materials for industrial success. Despite significant challenges such as lack of electricity, water scarcity, and inadequate infrastructure, Psaltry has achieved an annual income of $12 million. They strategically leveraged concessional loans from the Central Bank of Nigeria (CBN) through the Commercial Agricultural Credit Scheme (CACS) and Agricultural Credit Guarantee Scheme Fund (ACGSF) to fuel their growth and overcome critical operational challenges. Recognizing the alignment between their business stage and the funding requirements, Psaltry, in its early stages of scaling up, secured these loans at favourable terms which provided the necessary capital at favourable rates and allowed Psaltry to back local farmers with collateral guarantees. The concessional nature of the loans, with a single-digit interest rate, provided the necessary financial support to build their first starch factory in 2012, which was instrumental in establishing their production capabilities.

- Dayntee Farms – Non-traditional and Equity Financing (Expansion phase)

Dayntee Farms, established in 2012, is a Nigerian poultry farm with a comprehensive operation that spans the entire poultry farming value chain. The farm is involved in breeding day-old chicks, layers, and broilers, as well as hatchery operations, broiler fattening, and food processing. The farm leveraged its partnerships with smallholder and medium-scale farmers to finance inputs and services. By acting as an off-taker and out-grower for these farmers, Dayntee Farms established a reliable supply chain that allowed for the extension of credit and other financial arrangements within the network. They also utilised assets, such as livestock and equipment, as collateral to secure short-term credit lines. This provided the necessary liquidity to finance operations without relying on traditional bank loans. With improving business metrics, Dayntee Farms received a significant equity investment from Sahel Capital, the fund manager for the Fund for Agricultural Finance in Nigeria (FAFIN) in 2016 to support the expansion of the business production and distribution capacity. They successfully leveraged both traditional and non-traditional funding sources to maintain operational efficiency and scaling.

Future Outlook: Financing Trends in Agribusiness

Africa's food and agriculture industry is projected to be worth USD 1 trillion by 2030, up from USD 313 billion in 2010. This growth presents substantial opportunities for job creation, poverty reduction, and food security. However, financing remains a critical challenge for agribusinesses, particularly for working capital needs.

Traditionally, informal sources have been the primary means of financing for both farm and off-farm activities, with credit from input suppliers declining. Accessing credit from commercial banks has become increasingly difficult due to complex documentation and high lending rates, driven by unfavourable macroeconomic conditions. Market risks in on-farm operations deter most banks, especially when lending to smallholder farmers. Exceptions occur when smallholders are part of strong cooperatives or producer organizations, highlighting the need for cluster farming systems.

Most commercial bank lending in agribusiness is short-term, mismatching the long-term investment needs for machinery and infrastructure. This is compounded by banks' lack of specialized knowledge in agribusiness investments. However, an increasing number of investment funds, including private equity, venture capital, and impact investing, are targeting agribusinesses, often through public-private partnerships with development finance institutions (DFIs). These funds prioritize both development impact and profitability. Alternative financing models like crowdfunding and digital financial services, are also emerging, with the potential to revolutionize agribusiness financing, especially in regions with limited banking infrastructure.

With growing concerns about climate change, climate financing and green bonds are increasingly focused on supporting sustainable agricultural practices. Blended finance, which combines public and private investments, is becoming essential to de-risking agribusiness investments. Initiatives like the Nigeria Incentive-Based Risk Sharing System for Agricultural Lending (NIRSAL) are instrumental in bridging the financing gap for smallholder farmers.

To ensure sustainable growth, agribusinesses and governments must enhance financial literacy, strengthen public-private partnerships, adopt blended finance models, and leverage technology. By addressing these challenges, agribusinesses can thrive in an increasingly competitive global market.

How Vestance can Support your Fundraising Effort

At Vestance, we can position your agribusiness to secure the funding needed to thrive. Our services include:

- Capacity Development: Training in agricultural finance, risk management, cashflow management and financial planning to help you make informed decisions.

- Financial Modeling & Valuation: Developing robust financial models to assess project viability, identify risks and opportunities.

- Fundraising Support: Creating investor-ready business plans, financial models, and pitch decks, and connecting you with potential investors.

- Business Optimization: Streamlining operations and enhancing efficiency to maximize profitability.

- Market Research: Providing insights into market trends and opportunities to inform strategic decisions.

- Due Diligence: Conducting thorough assessments to secure your investments.

With our expert guidance, your agribusiness is positioned for growth and success. Schedule an appointment here